Housing affordability is a big issue for many Australians. Both the major parties claim to want to fix it, but neither has a plan to address the real causes of the crisis. Harry Chemay with the facts.

You know the housing market is in crisis when a high-flying investment banker and the CEO of an industry super fund make the same observations to the nation’s premier business publication.

Not natural allies by any stretch, one facilitates the pursuit of commercial profit-seeking, while the other represents some 3.5 million individuals hoping for a dignified retirement at some point in their lives.

Yet here they were, just days apart, with remarkably similar and profoundly disturbing insights into the woeful state of housing affordability in Australia today.

In early March, the CEO of Melbourne-based AustralianSuper, Paul Schroder, took to the stage at the AFR Business Summit and said this:

I think the big, burning productivity and cost of living problem is housing.

“I think we keep underestimating how worrying housing is. This is the crisis that is facing Australia.

“All we’ve done is pour all of this money into houses, which has deprived the economy of heaps and heaps of productive capital. We’ve got all this money in our domestic houses and we’re not backing business, we’re not creating new things, we’re not driving productivity.

“So, to me, all of our pants should be on fire about housing. Because, if our kids can’t live safely and securely, how can you be freed up to think positively about productivity or the future, if you don’t know where you’re going to live?”

About two weeks later, Jonathan Mott, a senior banking analyst at Sydney-based Barrenjoey Investment Bank, was on stage at the AFR Banking Summit and dropped more housing truth-bombs:

“Over the last three years, since we’ve started seeing rates go up, the lending to owner-occupier [households] who earn less than $120,000 per year (which is 60% of society) has fallen 66%. Only 8% of credit goes to owner-occupiers earning less than this.

At the same time, lending to investors earning more than $500,000 per annum is up 166%.

“This one percent of society is getting more credit [9% of mortgage lending] than the 60% who are owner-occupiers.

“This is not sustainable. If it doesn’t change and you live in Sydney, you’ll never know your grandkids, because they won’t be able to afford a house. They won’t live here.”

Both Schroder and Mott are experienced senior financial executives who can see today’s housing market for what it is: a brutal competition in which generally lower-to-middle income Australians are pitted against each other in a ‘housing hunger games’, either to rent from high-income investors or to buy from owner-occupiers (with the constant threat of being out-competed by better-funded investors).

A banker’s lament

Jonathan Mott’s concern about Sydney’s housing market has been validated by the just-released CoreLogic Home Value Index, which saw the median house price in the harbour city hit $1,472,393 during March, a new all-time high. Unit prices, meanwhile, rose to $851,934, 23% higher than the next most expensive capital city, Brisbane.

Mott is one of Australia’s most experienced banking analysts. He knows the role that mortgage lending plays in rocketing property prices, mortgage debt now sitting at some $3 trillion outstanding across homeowners and investors.

He would also undoubtedly be familiar with the current stats. The national average mortgage for a first-time home buyer is now around $520,000, while for existing owner-occupiers, it’s around $670,000 nationally and $811,000 in his home state of NSW.

Try servicing a 30-year $800,000 principal and interest mortgage at 6.25% pa on the median NSW household income of around $140,000. I calculate that to be just under $5,000 per month on a household take-home pay of around $9,500.

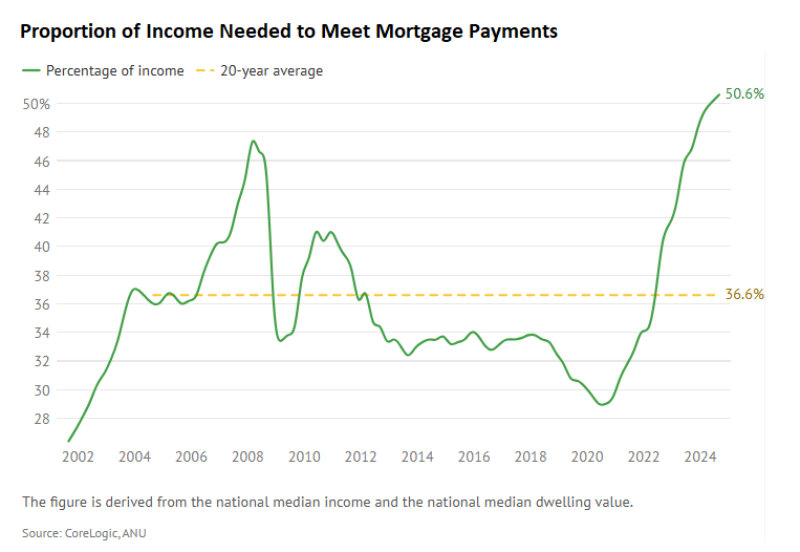

It’s little wonder that mortgaged households were caught out by the 2022-23 spike in official rates from 0.1% to 4.35% (before last month’s 0.25% cut). The proportion of household income needed to service a mortgage rose from under 30% in 2020 to now accounting for more than 50% of a typical mortgaged household’s budget.

That’s been a key cost-of-living drain for many of Australia’s roughly 3.7 million mortgaged households, who collectively owe around $1.5 trillion, particularly lower-income and younger borrowers.

If you engineer a system where homeowners are forced to take on ever-increasing levels of debt relative to their household incomes, they invariably face more interest rate risk. Alas, such is life in the mortgage nation that is Australia today.

Mortgage nation. The ‘wealth effect’ that drives big bank’s super profits.

Productivity and housing affordability

Paul Schroder’s focus at the AFR Business Summit was on productivity, that magical economic quantity said to drive our living standards. Productivity is, in essence, the amount of output each employee generates on average for each hour spent working.

More output per hour results, all else equal, in higher total national income and, in theory, the ability for employers to pay their workers higher salaries without consumer inflation becoming a concern ($).

Productivity is one of the ‘Three P’s’ in Treasury’s long-term GDP forecasting, alongside population and labour participation levels. Except productivity has essentially flatlined since 2016 and has actually been going backwards more recently.

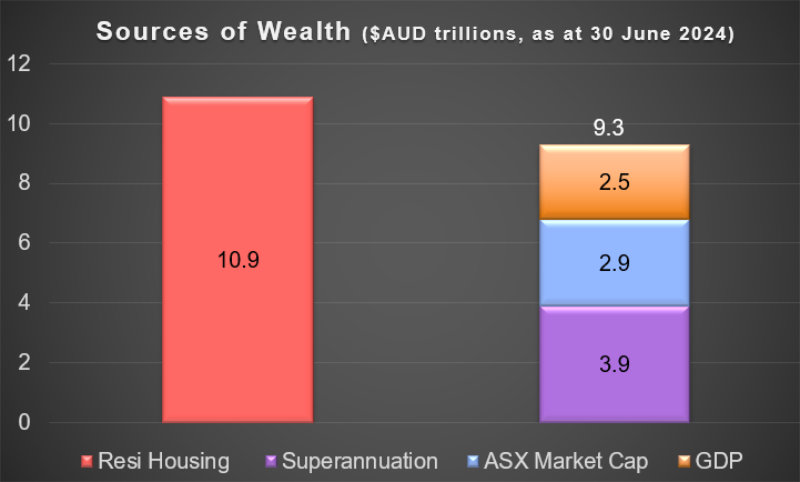

The AustralianSuper CEO identified a very likely contributor to the problem when he noted that our love affair with property sees Australia with a $11 trillion housing market and a $3 trillion GDP (almost 4X), versus a $50 trillion US housing market relative to its $29 trillion economy (about 1.7X).

Schroder’s argument that Australians over-save on residential property and deprive the productive economy of a domestic source of capital is valid. I made the same point in 2021 and again in a retirement conference last October to a room full of superannuation executives.

Source: ABS, APRA, ASX (author’s calculations)

You can take the entire Australian economy, add both the value of the ASX and the superannuation system,

and still be $1.6 trillion short of the wealth tied up in residential property.

That’s wealth currently held in non-productive land and buildings that could be used by Australian businesses to create Australian products and services, employ more Australians, and drive that elusive productivity lift.

Because even the Productivity Commission, in its recent deep dive into housing construction productivity, admitted that we get half as much house per construction hour worked than we did three decades ago. If productivity growth is indeed the path to economic prosperity for all Australians, then perhaps continuing to bank on residential property is not the long-term road there.

Trade tension impact

Something to think about in a post ‘Liberation Day’ world; a world where rising trade tensions will put the focus squarely back on productivity, and in finding ways to support Australian businesses to compete, grow, employ and generate rising incomes.

Being leveraged up to the eyeballs to own property might provide the illusion of wealth (the RBA itself accepts that a ‘wealth effect’ exists here), but it won’t do much to raise long-term living standards for working Australians.

And approaching retirement with mortgage debt, as one in two households aged between 55 and 64 now do, won’t help living standards thereafter either. That’s the legacy of real mortgage debt for those over 55 increasing by more than 600% between 1987 and 2015.

It’s a game of property snakes and ladders that Australia has played over the last 25 years. A game that, as Mott correctly asserts, is patently unsustainable.

Snakes and Ladders: stimulus schemes and debt skew economy as property prices rocket

Harry Chemay has more than two decades of experience across both wealth management and institutional asset consulting. An active participant within the wealth and superannuation space, Harry is a regular contributor to investment websites in Australia and overseas, writing on investing and financial planning.