Fees garnered from household expenditure increased by 11% last financial year, mainly from personal loans and credit cards, according to the Reserve Bank. Bank fee gouging is ubiquitous, Andrew Gardiner reports.

Are you noticing more and more fees and charges popping up (or not popping up, as can be the case) on your bank statements? The ones many of us ignore because they’re a ‘pittance’, not worth chasing up?

It turns out they’re worth billions to big banks, with experts worried we’ll grudgingly accept them because they’ve crept up on us incrementally, have become ‘normal’ and – on a transaction-by-transaction basis – are just so damned trifling.

It’s not a bug, it’s a feature, they say: part of a deliberate movement towards ubiquitous micro-payments we barely notice in what’s fast becoming a cashless society. “Banks see revenue streams from fees as the way of the future,” bank victims advocate Geoff Shannon told MWM.

Smarting from the black eye they got on lending practices during the Global Financial Crisis (GFC, 2007-08) from the Banking Royal Commission (BRC), Australia’s banks have slowly ceded ground on their market dominance of finance. Loans, once a near-monopoly for the Big Four, are moving towards an ‘open slather’ situation for second and third-tier lenders like Pepper Money or FirstMac.

While not subject to any new rules and regulations following the BRC, big banks made an effort to ensure there wouldn’t be any changes to the law by self-regulating, abandoning cowboy lending practices and generally making it harder for them to do business. With those ultra-lucrative net interest margins now a diminishing component on their profit and loss reports, banks were desperate for an alternative revenue stream.

They appear to have found one: us.

The cashless society

As we’ve moved inexorably towards a cashless society, we’re seeing banks move to impose fees and charges on seemingly everything imaginable. “If the banks can clip the ticket, they’ll do it,” Shannon told MWM.

COVID, with its mandatory no-contact payments, was a fortuitous moment for the banks, rendering cashless payments a normal and accepted way of life that, for the most part, we haven’t sought to shake. “Many of these fees are hidden away in fine print or hard to discern on bank statements. When a transaction doesn’t involve cash in your hand, it’s that much easier to obfuscate,” Shannon pointed out.

For credit and debit cards, there are also monthly (or annual) fees, additional cardholder fees, cash advance fees, late payment fees, international transaction fees, over limit fees, replacement card fees, minimum balance fees, paper statement fees, online billing fees and my personal favourite, insufficient funds fees.

And let’s not forget the medley of fees Australians pay if they’re still taking out bank loans. It all adds up.

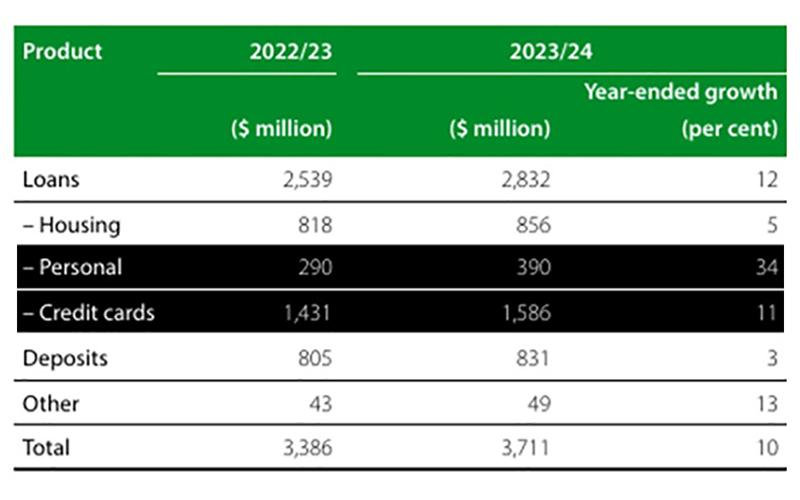

Fees from personal loans and credit cards were a major source of revenue for banks in 2023-24. Source: Reserve Bank.

The most recent shift towards fees as a revenue raiser came from credit cards and personal loans.. An 11% per cent increase in credit card fees for 2023-24 mainly came from foreign currency conversion fees, but on a more rapacious note, the 34 per cent growth around personal loans came to a large extent from establishment fees imposed on people who, in a difficult year, may be taking out the loans as a quick fix against soaring inflation and mortgage interest rates.

Perhaps the banks’ most egregious imposition comes in the form of surcharges on small business operators at the point-of-sale. Passed on to consumers, you can simply not notice them because they’re not printed on price tags or, often, not clearly specified in statements.

Say you go to a kebab shop in Brunswick or Newtown, and the sign says $8.50 for Turkish bread. If a surcharge is applicable, you’ll actually have, say, $8.60 debited from your card, and chances are you won’t even notice it, either then or when your statement comes. “That kind of thing happens all the time, and people are often completely in the dark,” forensic accountant Jeff Knapp told MWM.

Surcharges on the falafels might seem insignificant, but here’s the kicker: across the economy, on transactions large and small, they cost us $4B a year. Labor MP Jerome Laxale told Parliament,

we’re each paying hundreds of dollars annually to use our own money.

“Paying for things used to be free, and for those of us who still use cash, it still is,” he said. But cash now accounts for only 13 per cent of transactions.

Cowboy loans

Big banks might be self-regulating these days, but the predatory lending practices that led to the BRC haven’t simply vanished. Instead, they’ve been eagerly embraced by some second and third-tier lenders, unburdened by either conscience or regulations (on business loans in particular) that the BRC was supposed to help spawn.

These days, the cowboys are simply smaller … as are their victims, in many cases. Family-run businesses in need of a ‘quick fix’ of cash in a tough economy are heavily represented among victims.

In a fix with creditors, they sign up for contracts they don’t understand, which lands them in worse debt than before. Shannon, who works with many such victims, says that in some cases, the interest rates and fees charged have been up to 200%.

“I had one client having to pay back $3,000 per day for $265,000 in loans. That’s $450,000 they had to repay, which simply isn’t viable,” he told MWM.

It’s nothing short of loan sharking.

Insolvency is often inevitable when taking out these cowboy loans, with the building and construction sector among the worst affected. In 2024, the Australian construction industry saw a significant increase in insolvencies compared to 2023, with 2832 construction companies undergoing insolvency appointments, a 28% rise from the previous year, according to the AFR ($).

Many of those are small businesses that are not protected under responsible lending laws, which only apply to individual consumers.

Shannon wants the law changed to ensure these smaller businesses and their guarantors fall within tighter consumer law protections. “Until that happens, they will keep getting devoured by these predators,” he said.

But extending the law to cover small businesses poses problems of its own. It could, in turn, mean lenders back away from offering finance to small businesses, just as banks recoiled from some forms of finance after their bruising by the BRC.

Assistant Treasurer Stephen Jones is reluctant to make changes for that very reason: “We don’t want to lock people out of credit”, he told the ABC.

Small business owners remain emotionally on the precipice, meaning Geoff Shannon’s role is as much a counsellor as an advocate. He founded Unhappy Banking, whose website provides a fair summary of his own personal feelings: “We’re mad as hell about banks treating ordinary Australians poorly, often instigating repossession of property to suit their hidden corporate agenda.”

“I’ve literally talked people down” from suicide, he told MWM.

And agendas are what this whole shift in our financial system is all about, Shannon says. He’s keen to disabuse the more naïve among us of the notion this viral spread of fees and surcharges, and banks ceding predatory lending practices to smaller operators, “just happened.”

It’s not happenstance, he says. “After the GFC, it was planned all along.”

CommBank’s Matt Comyn, ASIC face mal-prosecution claims from Unhappy Banking founder Shannon

An Adelaide-based graduate in Media Studies, with a Masters in Social Policy, I was an editor who covered current affairs, local government and sports for various publications before deciding on a change-of-vocation in 2002.